⚠️ Affiliate Disclosure: We earn a commission on purchases made via our links — at no extra cost to you.

Is Your Double Discount Coupon Actually Saving You Money?

Contents

hide

Walk into any online sale today and you will notice something interesting. Discounts are no longer simple. Gone are the days of a single flat price cut. Instead, shoppers are now presented with layered offers like “25% off plus an extra 10% at checkout” or “flat discount plus bank cashback.” At first glance, these deals appear extremely generous. The numbers feel large, and the perceived savings feel even larger. But beneath that surface lies a subtle mathematical reality that most people overlook.

The truth is, many shoppers today are not actually saving as much as they believe. They are estimating instead of calculating. And in finance, estimation without understanding often leads to poor decisions. This is exactly where a double discount calculator becomes more than just a tool. It becomes a mindset shift.

Understanding how discounts truly work is not about being good at math. It is about being aware of how money moves. And once you understand that, every shopping decision becomes sharper, more intentional, and more aligned with your financial priorities.

The Invisible Math: How a Double Discount Coupon Actually Layers Savings

At its core, a double discount is deceptively simple. It is not the sum of two discounts. It is the application of one discount followed by another, each acting on a different base.

This distinction is where most confusion begins.

When you see two discounts together, your brain naturally wants to combine them. It feels intuitive to say that 20% plus 10% equals 30%. But financial systems do not operate on intuition. They operate in sequence.

The first discount reduces the initial price. The second discount then applies to the new price, not the original one. This means the second reduction is always smaller in absolute value than the first, even if the percentage looks significant.

A helpful way to visualize this is to imagine peeling layers off an object. Each layer removed exposes a smaller surface underneath. You are not removing everything at once. You are removing it step by step. That is exactly how a double discount works.

Psychology of the Stack: Why Retailers Love the Double Discount Coupon Illusion

There is a reason retailers prefer stacking discounts instead of offering one large percentage. It is not accidental. It is psychological.

Multiple discounts create the illusion of a bigger deal. They trigger a sense of urgency and excitement. When a shopper sees an extra 10% off, it feels like a bonus. It feels like an opportunity that should not be missed.

But from a financial perspective, this structure benefits the seller just as much as the buyer. Because when discounts are applied sequentially, the total discount is always slightly lower than the simple addition of percentages.

This small difference is where businesses protect their margins. And this is exactly where informed shoppers gain an advantage by choosing to calculate instead of assume.

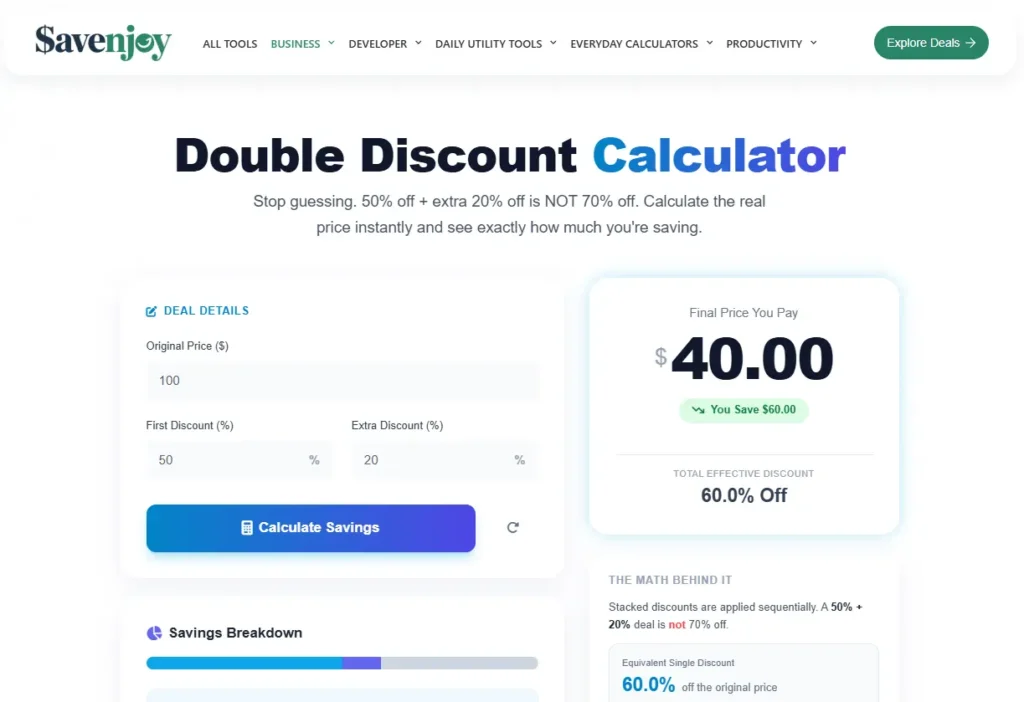

Why a 20% Double Discount Coupon is Not What You Think: Decoding the Math

Let’s address the most common misunderstanding directly. A 30% discount followed by a 10% discount does not equal 40%.

To understand why, you need to follow the actual flow of numbers rather than rely on mental shortcuts.

Imagine an item with an original price of 1000. The first discount reduces it by 30%. That brings the price down to 700. Now the second discount of 10% applies, but not to 1000. It applies to 700. This results in a reduction of 70, bringing the final new price to 630.

What you have saved is 370, not 400. The effective discount is 37%, not 40%.

This difference may appear small in isolation, but over time, especially with larger purchases, it becomes significant. It directly affects your expenses, your ability to set aside money, and your progress toward any long term goal you may have.

The Logic Behind the Formula

To remove ambiguity, financial analysts rely on a structured approach rather than repeated step-by-step calculations. This is where the standard formula comes into play:

Price_new = Price_initial × (1 − r) × (1 − q)

Here, each discount is converted into a decimal. This is important because percentages must be translated into a format that can be multiplied.

For example, 20% becomes 0.20 and 10% becomes 0.10. Once converted, the calculation becomes a simple multiplication process. This ensures accuracy and eliminates guesswork.

Imagine you are buying a high-end MacBook Pro for your business. You’ve been tracking the price, and today is the day to buy.

- Original Price: $2,500

- Store Sale: 20% OFF

- Special Coupon: Extra 10% OFF at checkout.

The Common Shopper Assumption:

Most people think: $20% + 10% = 30%$ Savings.

- Expected Discount: $30% of $2,500 = $750

- Expected Final Price: $1,750

The Reality:

- First Discount (20%): $2,500 – $500 = $2,000$

- Second Discount (10% on $2,000): $2,000 – $200 = $1,800

The Hidden Cost of Estimation:

- The Difference: $50

- The Effective Discount: 28% (Not 30%)

The power of this formula lies in its consistency. Whether you are dealing with two discounts or three, the logic remains the same. You simply continue multiplying the remaining value after each reduction.

This is exactly how a double discount calculator operates behind the scenes. It does not think. It follows a precise mathematical sequence.

From Double to Triple Discounts: When Complexity Increases

![A professional digital infographic showcasing a home electronics triple discount stack, with a large bold 'SAVE UPTO 45% OFF' headline, and detailed subtext 'Home Electronics Multi-Deals: Get 35% OFF + Extra 10% + Bonus 5% ON Orders $300+'. A blue 'SHOW COUPON CODE' button reveals two masked codes [ST...10] [TR...5]. A list of five bullet points details the conditions, including a 35% event discount, a stacked 10% off code, a bonus 5% off code, a maximum $75 cap, and refined exclusions. The graphic includes verification, usage count, a five-day expiry timer, and like/share icons against a white background.](https://savenjoy.com/wp-content/uploads/2026/03/Home-Electronics-Multi-Deals-Coupon-Card-%E2%80%93-Save-Upto-45-OFF-1024x426.png)

As online shopping evolves, discounts are becoming more layered. It is now common to encounter situations where three different benefits apply to a single purchase.

A typical example might include a seasonal sale, a coupon code, and a cashback offer. Each of these operates differently. Some reduce the price immediately, while others return a portion of the cost later.

This creates a more complex structure where the order of application and the type of discount both matter. A cashback, for instance, does not reduce the purchase price at checkout. It impacts your net spending afterward.

This is where many shoppers miscalculate their real savings. They combine all percentages mentally without considering when and how each discount applies.

In such scenarios, a disciplined step-by-step approach becomes essential. Without it, the perceived savings can differ significantly from the actual outcome.

Let’s explore a situation. Imagine you are upgrading your home office or entertainment center. You find a high-end setup originally priced at $5,000.

The Triple Offer:

- Holiday Markdown: 20% OFF (Store-wide sale)

- Loyalty Coupon: Extra 10% OFF (Member exclusive)

- Credit Card Cashback: 5% BACK (Statement credit)

Most of us will guess: $20% + 10% + 5% = 35% Total Savings.

- Assumed Saving: $35% of $5,000 = $1,750$

- Assumed Final Cost: $3,250

The Reality:

In credit card cashback, We apply each discount to the remaining balance, layer by layer:

- Layer 1 (20% Sale): $5,000 – $1,000 = $4,000$

- Layer 2 (10% Coupon on $4,000): $4,000 – $400 = $3,600

- Layer 3 (5% Cashback on $3,600): $3,600 – $180 = $3,420

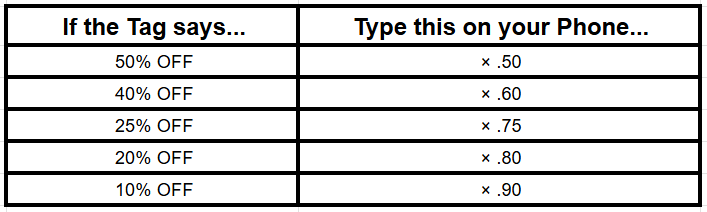

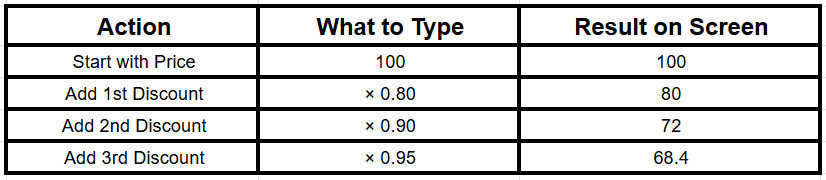

How To Calculate Triple Discount Coupons on a Calculator?

I have created a beautiful table for you. I promise you’ll learn to calculate once you go over the below picture.

Since you know what you have to pay and got the decimal number. I’ll show you how to calculate on a calculator.

The simple formula is Price ×0.80×0.90×0.95= your answer.

Suppose price = $100 (100×0.80×0.90×0.95= $68.40)

The Real Impact on Personal Finance

Discounts are often seen as opportunities to save money. But in reality, they influence consumer behavior more than they influence finances.

A discount can easily shift your mindset from”Do I need this?” to “This is a good deal.” That shift is subtle but powerful. It can lead to increased spending under the illusion of saving.

From a financial perspective, the goal is not to maximize discounts. It is to optimize outcomes. This means understanding how each purchase fits into your overall financial picture.

Your income defines your limits. Your expenses define your flexibility. And your savings goal defines your future.

Every purchase should ideally support that structure. Discounts should help you spend less on what you already need, not justify spending more on what you do not.

Developing a Smarter Shopping Approach

The most effective shoppers are not those who chase the biggest discounts. They are the ones who approach every deal with clarity.

This begins with intention. Before looking at any discount, you should already know whether the purchase aligns with your needs. Once that is clear, the next step is evaluation.

Instead of focusing on the percentage displayed, focus on the final number. The only number that truly matters is the amount you will actually pay.

This is where tools like a regular discount calculator or a double discount calculator become valuable. They remove ambiguity and allow you to compare options objectively.

Another important habit is to mentally convert savings into opportunity. If you save a certain amount, consider what that amount could contribute toward your future. Could it be invested? Could it be added to a financial cushion? Could it support a larger goal?

This shift in thinking transforms savings from a short-term benefit into a long-term advantage.

Why Accuracy Matters More Than Ever

In today’s digital shopping environment, decisions are made quickly. Flash sales, limited-time offers, and countdown timers create urgency. Under such conditions, mental math is often unreliable.

This is why relying on precise calculation is not just helpful, it is necessary. A small error in understanding a discount can lead to repeated misjudgments over time.

A double discount calculator solves this problem by providing instant clarity. It allows you to make decisions based on facts rather than assumptions. And in finance, clarity always leads to better outcomes.

Conclusion:

At first glance, discounts appear to be about saving money. But at a deeper level, they are about decision-making.

Understanding how double discounts work gives you more than just mathematical accuracy. It gives you control. It allows you to see through marketing tactics and focus on what truly matters.

Because ultimately, financial strength is not built through occasional savings. It is built through consistent, informed choices.

And once you begin to calculate instead of assume, you stop being influenced by discounts and start using them to your advantage.

FAQs

- Does the order of discounts matter?

From a mathematical perspective, when both discounts are percentages, the order does not change the final result. However, in real-world scenarios involving cashback or conditional offers, the sequence can affect the outcome. - Is a double discount always better than a single discount?

Not necessarily. A single higher percentage discount can sometimes provide greater savings than two smaller sequential discounts. The only reliable way to know is to calculate the final price. - How can I quickly determine the real discount?

The most efficient way is to use a double discount calculator or apply the formula by converting percentages into decimals and multiplying step by step. - What is the difference between total savings and effective discount?

Total savings refers to the actual amount of money reduced from the original price, while effective discount represents that saving as a percentage of the initial price.

Hi, I am Priyanka Roy, an SEO Specialist and Content Writer at Sandhu Marketing Agency Inc.. For the past 4 years, I have been helping businesses improve their websites and grow their organic traffic through practical and effective SEO strategies.

I enjoy working on different SEO tools and exploring how they actually perform in real situations. Over time, I have tested many tools, faced real challenges, and learned what works and what does not. This is exactly what I share on Savenjoy. My goal is to help you understand what to expect from a tool before you spend your money on it.

Instead of just listing features, I focus on real experiences, honest insights, and simple explanations so you can make better decisions with confidence. All I want is to make your journey easier and smarter.

I love trying new digital tools even when I do not need them, just to see if they are worth it or not.